How much does car insurance cost in the USA in 2026?

How much does car insurance cost in the USA in 2026? Your renewal notice just landed in your inbox — and the number staring back at you feels way too high. You’re not imagining it. Premiums have jumped roughly 18% over the past year. But before you accept that bill without question, you deserve to know exactly what the numbers look like, why they are what they are, and what you can realistically do about it.

Let’s be real: nobody enjoys shopping for car insurance. But ignoring the cost — or just auto-renewing without a second look — is one of the most expensive things you can do as a driver in 2026. Rates have climbed sharply, but the gap between the most expensive and cheapest quote for the exact same driver can exceed $500 a month. That means comparison shopping isn’t optional anymore. It’s essential.

How much does car insurance cost per month in the USA?

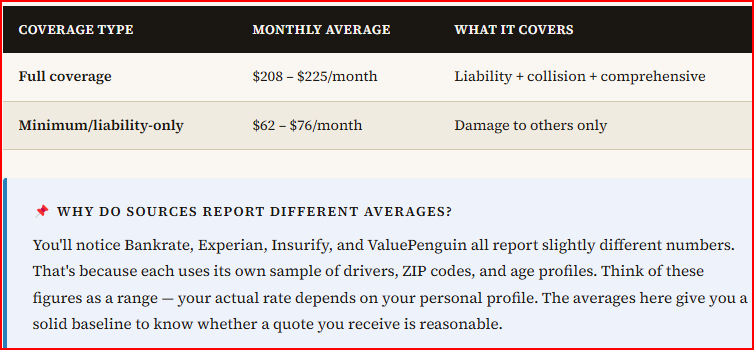

The short answer: it depends almost entirely on what kind of coverage you buy. There are two main tiers — minimum (liability-only) coverage and full coverage — and the price difference between them is dramatic.

Full coverage is a combination of three policy types: liability (which pays for damage you cause to others), collision (which covers your own car after a crash), and comprehensive (which handles theft, weather, fire, and other non-collision events). If your car is financed or leased, your lender almost certainly requires it.

Minimum coverage, also called liability-only, only pays for damage you cause to someone else. It does not pay to repair your own vehicle. It’s the bare legal minimum required to drive in 49 states (New Hampshire is the exception).

One thing worth noting: rates are finally stabilizing. After a brutal 26% surge in 2024, the pace of increase has slowed dramatically. Analysts at ValuePenguin and Insurify both project just a 0.67% national rate increase for 2026 as a whole — a meaningful relief signal, even if your wallet still feels the effects of the past few years.

There’s one wild card, though: trade tariffs. A 25% tariff on imported vehicles took effect in April 2025, followed by a 50% increase on foreign aluminum and steel. When replacement parts cost more, insurers eventually pass those costs on through higher premiums. Watch for this to show up in renewal notices throughout 2026.

How much does car insurance cost per year in the USA?

Stretched across 12 months, the numbers feel even more real. On an annual basis, full coverage averages between $2,496 and $2,697, while minimum coverage runs $820 to $912 per year, depending on the data source. That’s a meaningful chunk of any household budget.

+18%Average increase in U.S. car insurance premiums from 2025 to early 2026, per The Zebra — January 2026 data.

What makes your personal annual rate go up — or down — more than anything else? Here are the factors that insurers weigh most heavily:

Age and experience

This is the biggest swing factor. A 16-year-old pays an average of $5,757 per year for full coverage. A 60-year-old pays around $2,411 per year — less than half. Teen drivers represent statistically higher risk, and insurers price accordingly. Rates drop steadily through your 20s and 30s, bottom out around age 60, and then begin ticking back up in your mid-70s.

Your driving record

A clean record saves you roughly 7% below the national average. But violations stack up fast. A single speeding ticket raises your rate by an average of 22%. An at-fault accident pushes your monthly full-coverage payment from $225 to $322. A DUI (driving under the influence) conviction is the most costly: it doubles your rate on average — a 96% increase — and can follow you for 10 years in many states.

Your credit score

In 47 states, insurers use a credit-based insurance score as a rating factor. Drivers with poor credit pay nearly 76% more for full coverage than those with good credit. California, Hawaii, and Massachusetts are the exceptions — state law prohibits insurers there from using credit as a factor. If you’re in any other state and carrying debt, this could be meaningfully inflating your premium.

What you drive

The Toyota RAV4 and Honda CR-V are the most affordable new vehicles to insure in 2026, averaging around $214 per month — about 14% below average for popular 2025 models. At the other end, the Tesla Model Y costs an average of $354 per month to insure, largely because of its repair costs and parts pricing. Electric vehicles (EVs) from legacy automakers like Chevrolet and Ford now cost about 49% less to insure than those from EV-only brands like Tesla and Rivian.

Gender and marital status

In states where gender is an allowed rating factor, men pay slightly more than women — an average of $2,297 versus $2,272 annually, per Experian data. The reasoning, according to the Insurance Information Institute, is that men are statistically more likely to engage in high-risk driving behaviors. Married drivers also tend to receive lower rates than single drivers, as data suggests they file fewer claims.

💡 Good to know

A 6-month policy for a household with a teen driver averaged $2,846 in January 2026, per The Zebra. Adding a teen to your policy is expensive — but a few strategies can help, which we cover in the expert tips section below.

Car insurance cost by state in the USA

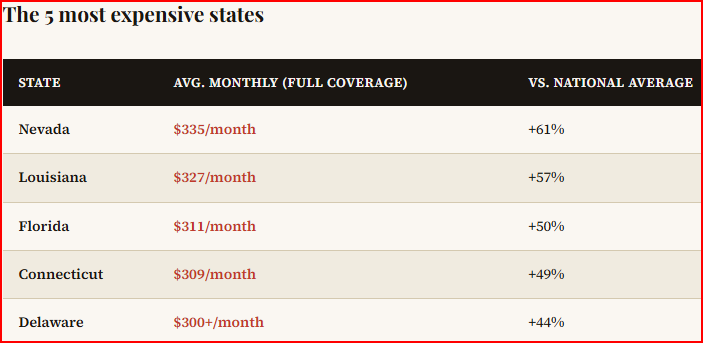

Where you live matters enormously. The most expensive state for car insurance in 2026 costs more than two and a half times the cheapest. That difference isn’t random — it reflects real local conditions: traffic density, weather events, the cost of labor and parts, how many uninsured drivers are on the road, and the specific liability minimums your state requires by law.

Florida’s high rates come from a perfect storm of factors: a no-fault insurance law, high litigation rates, extreme weather events (hurricanes, flooding), and one of the highest rates of uninsured drivers in the country. Nevada’s dense urban driving in Las Vegas, combined with high vehicle theft rates, drives its costs up similarly.

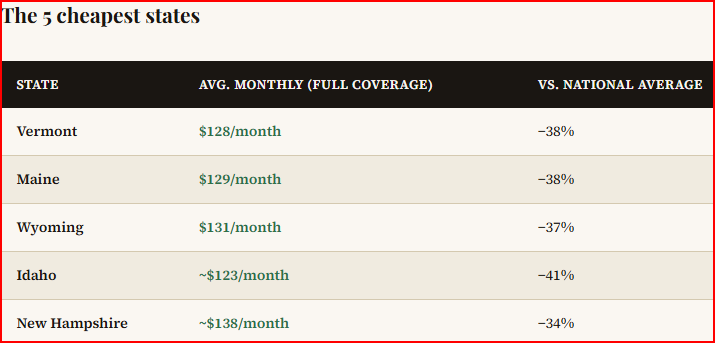

These rural states share common traits: low population density, fewer accidents per mile driven, lower vehicle theft rates, and lower labor costs for repairs. Vermont and Maine also benefit from relatively mild litigation environments — fewer lawsuits following accidents means lower costs for insurers, savings that trickle down to you.

⚠️ Heads up if you live in New Jersey

New Jersey drivers face some of the steepest projected rate increases in 2026 — an estimated 10.46% hike when policies renew, according to ValuePenguin. If you’re in New Jersey, now is the time to comparison shop before your renewal date arrives.

Who has the cheapest car insurance in the USA?

The cheapest insurer for your neighbor may not be the cheapest for you. Rates are deeply personal — they change based on your age, ZIP code, vehicle, and driving history. That said, some companies consistently undercut the national average across a wide range of driver profiles.

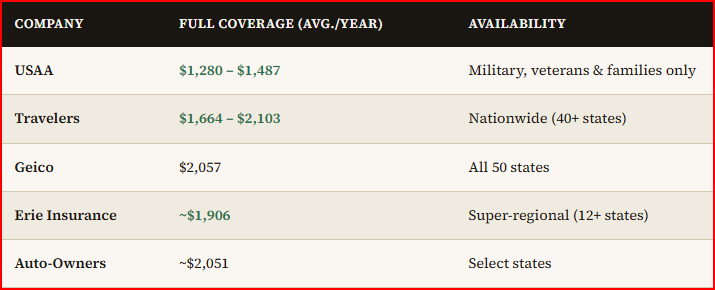

USAA is almost always the cheapest option available — but it’s limited to active military members, veterans, and their immediate families. If you qualify, there’s rarely a reason to go elsewhere.

For everyone else, Travelers is the cheapest large national insurer for full coverage, averaging $139/month per NerdWallet’s May 2026 analysis. Geico wins for minimum/liability coverage, coming in at just $41/month for liability-only, according to the same analysis.

Don’t overlook regional carriers. Erie Insurance, available in about a dozen states, averages just $159/month for full coverage — lower than any national carrier. If Erie operates in your state, it’s worth including in your quote comparison. Similarly, Farm Bureau, Westfield, and Farmers Mutual of Nebraska regularly price 20%–30% below national brands in their coverage areas.

💡 The single most valuable action you can take

Drivers who compare quotes from multiple insurers save an average of $480 per year. The spread between the cheapest and most expensive company for the same driver can exceed $500 per month in some states. Getting three to five quotes at renewal isn’t just smart — it’s one of the highest-return 10 minutes you can spend.

Myth 01

“Minimum coverage is enough protection”

Legally sufficient is not financially safe. If you cause a serious accident and your liability limits are exhausted, you pay the rest out of pocket — potentially losing savings, property, or future wages. Liability minimums vary wildly by state and many are dangerously low.

Myth 02

“Your credit score doesn’t affect your rate”

In 47 states, it absolutely does. Poor credit can raise your full-coverage premium by nearly 76% compared to good credit. Insurers use a credit-based insurance score — separate from your standard credit score — to assess claim risk. Only California, Hawaii, and Massachusetts prohibit this practice.

Myth 03

“Older cars are always cheaper to insure”

Not necessarily. A classic or collectible vehicle may require agreed-value coverage that costs more than a standard policy. Older cars that lack modern safety features (automatic emergency braking, lane-keeping assist) may also carry higher rates because they’re more likely to cause injury in a crash.

Myth 04

“Loyalty discounts mean you shouldn’t switch”

Loyalty discounts sound good — and they can be — but the average driver who switches saves $480 per year. Insurance companies often raise rates at renewal while their discounts stay flat. Always get outside quotes before you renew, even if you’re happy with your current insurer.

Myth 05

“All quotes for the same coverage are roughly equal”

This couldn’t be further from the truth. In Connecticut, the cheapest full-coverage insurer (Travelers) charges about $127/month while the most expensive (Hanover) charges more than five times that amount — for the same driver profile. The gap is real, and comparing quotes is how you find it.

Myth 06

“EVs cost a lot more to insure than gas cars”

This used to be true, but the gap is closing fast. In 2026, EVs from legacy manufacturers like Chevrolet, Honda, and Ford cost only about 4%–10% more to insure than their gas equivalents. The Chevrolet Equinox EV averages just $226/month — only slightly above average for new vehicles.

Expert tips to lower your car insurance premium in 2026

Knowing the average is useful. Knowing how to beat it is better. These strategies are used by savvy drivers — and recommended by licensed insurance professionals — to meaningfully reduce premiums without sacrificing coverage quality.

Tip 01

Shop every 6–12 months

Set a calendar reminder at renewal time. Request quotes from at least three to five companies using your exact driver profile. Never auto-renew without checking the market first — even one competing quote could save you hundreds.

Tip 02

Bundle home and auto

Purchasing your homeowners or renters insurance from the same provider as your car insurance can save you up to 25%. Most major insurers offer multi-policy discounts that apply automatically when you bundle.

Tip 03

Opt into telematics programs

Programs like Progressive’s Snapshot, State Farm’s Drive Safe & Save, and Geico’s DriveEasy track your driving habits via an app or device. Safe drivers typically save 10%–30% on their premiums. If you’re a calm, low-mileage driver, this is one of the easiest wins available.

Tip 04

Raise your deductible

Your deductible is what you pay out of pocket before insurance kicks in. Raising it from $500 to $1,000 can meaningfully lower your monthly premium. Just make sure you have that amount in savings before you make the switch.

Tip 05

Improve your credit score

In the 47 states where credit-based insurance scores are allowed, paying down debt and correcting errors on your credit report can lower your rate by a meaningful amount. Even moving from “poor” to “fair” credit can reduce premiums by tens of dollars per month.

Tip 06

Stack every discount you qualify for

Most insurers offer discounts you’ll never hear about unless you ask. Common ones include: good student discount, homeowner discount, paid-in-full discount (paying your 6- or 12-month premium upfront), low-mileage discount, and defensive driving course completion. Geico alone offers 16 separate discounts.

Tip 07

Drop full coverage on older paid-off vehicles

If your car is worth less than 10 times your annual premium, full coverage may no longer make financial sense. A car worth $4,000 insured for $2,500 a year in full coverage means you’re paying nearly the car’s value every two years for protection. Liability-only may serve you better.

Tip 08 — For parents of teen drivers

Get your teen’s license early

Insurers price risk partly based on how long someone has held a license. Getting your teen licensed as soon as legally possible — even if they won’t drive solo for a while — starts the clock on their experience. Every year further from “just licensed” brings their rate down. State Farm’s Steer Clear Program and Auto-Owners also offer strong discounts for new young drivers.

Key takeaways

- The national average for full coverage car insurance in 2026 is roughly $208–$225 per month ($2,496–$2,697/year). Minimum coverage averages $62–$76 per month.

- Premiums jumped ~18% from 2025 to early 2026, but the pace of increase is slowing sharply — analysts project just 0.67% additional growth for the rest of 2026.

- Where you live has a huge impact. Nevada ($335/mo) costs more than 2.5 times Vermont ($128/mo) for the same full-coverage policy.

- USAA is the cheapest insurer overall — but only for military members and their families. Travelers leads for the general public on full coverage. Geico leads for minimum coverage.

- Your driving record, credit score, age, and vehicle type are the four biggest levers on your personal rate — and some of them you can actually control.

- A DUI conviction raises your average rate by 96%. A single speeding ticket raises it by 22%. A clean record is worth protecting.

- Comparison shopping saves drivers an average of $480 per year. Never auto-renew without getting at least three competing quotes first.

- Bundling home and auto insurance can save up to 25%. Telematics programs can save 10%–30% more for safe drivers.

The bottom line

Car insurance in 2026 is expensive — there’s no sugarcoating that. But the good news is that you have more control than you might think. The averages in this guide give you a baseline. Now your job is to use them. If your current quote is significantly above the national average for your coverage type, that’s a signal worth acting on.

Start with three to five quotes from a mix of national and regional insurers. Ask every company about discounts you might qualify for. Consider telematics if you’re a calm, low-mileage driver. And if you’re carrying full coverage on a car that’s worth very little, crunch the numbers — you may be paying for protection that costs more than the car itself.

You now know what car insurance should cost in 2026. The next step is simple: find out what it actually costs for you — and if those numbers don’t match up, do something about it.