Are Real Estate Taxes and Property Taxes the Same in the USA? If you’ve recently purchased a home—or are planning to—you’ve likely come across the terms real estate taxes and property taxes on your mortgage statement, tax forms, or insurance documents. Are they the same thing? In most everyday contexts, yes—but there are important distinctions every U.S. homeowner should understand.

Are Real Estate Taxes and Property Taxes the Same in the USA?

This guide breaks down everything you need to know: what these taxes are, how they are calculated, how they appear on your IRS forms, how to reduce them, and how they connect to your homeowners insurance. All information is sourced from official U.S. government publications.

|

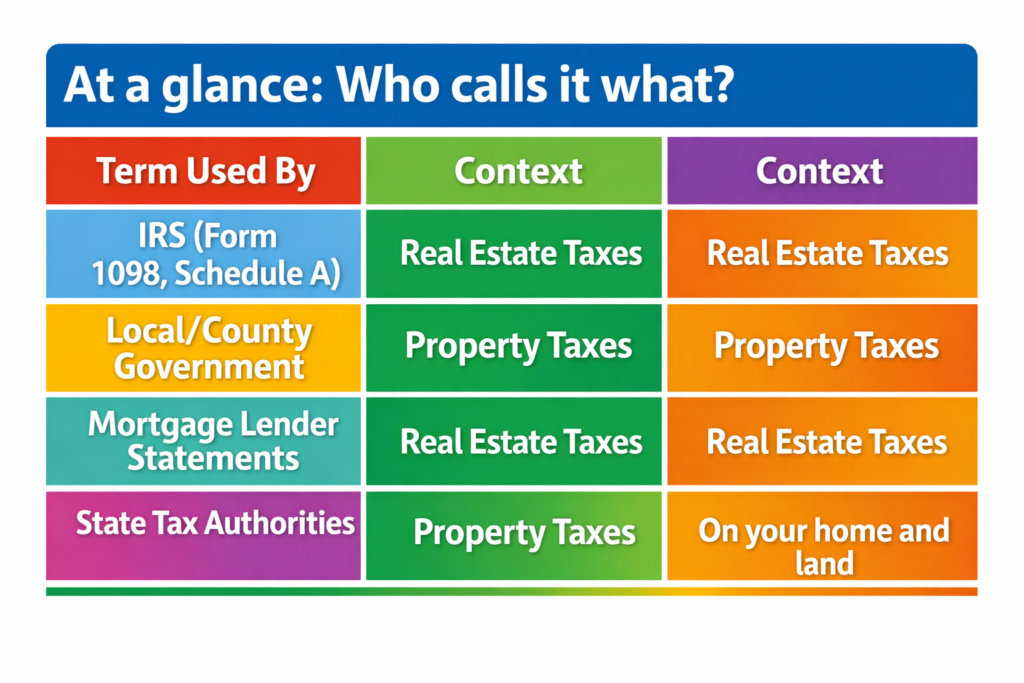

✅ Quick Answer Real estate taxes and property taxes refer to the same tax in most U.S. homeownership situations. Both fund local services such as public schools, fire departments, and roads. The IRS uses the term “real estate taxes” on official forms; local governments typically say “property taxes.” They are the same levy. |

1. Real Estate Taxes vs. Property Taxes: What Is the Difference?

In the United States, the two terms are used interchangeably for taxes on land and the buildings attached to it. When your county assessor’s office refers to a “property tax” and your mortgage lender refers to “real estate taxes” on your escrow statement, they mean the same thing.

The one technical distinction: In some states, “property tax” can also cover personal property—such as vehicles, boats, or business equipment—in addition to real estate. “Real estate taxes,” however, refer exclusively to taxes on land and permanent structures.

According to the IRS, real estate taxes are defined as “state, local, and foreign taxes on real property.” [1] This is the tax that funds essential community services in your area.

2. How to Find Out How Much Your Property Tax Is?

There are several reliable ways to locate your exact property tax amount:

Check Your Monthly Mortgage Statement

If you have an escrow account, a portion of every monthly payment goes toward property taxes. Your annual mortgage statement provides a year-end summary of all taxes paid on your behalf. Look for the line item labeled real estate taxes or property taxes in the escrow breakdown.

Review Form 1098 from Your Mortgage Lender

By January 31 each year, your mortgage servicer is required to send you IRS Form 1098 (Mortgage Interest Statement). Box 10 on this form shows the exact amount of real estate taxes your lender paid on your behalf during the prior calendar year. [3]

Visit Your County Assessor’s or Treasurer’s Website

Most counties maintain a publicly searchable online portal. You can look up your property by:

- Street address

- Owner name

- Parcel number (APN) or Tax ID

These portals show your assessed value, applicable tax rate, taxes owed, and payment history.

Contact Your Local Tax Authority Directly

When in doubt, call your county assessor’s office (for assessed values) or your county treasurer or tax collector’s office (for payment amounts and deadlines). According to USA.gov, local tax offices are the official source for property tax information in your jurisdiction. [5]

| 📌 How Your Tax Is Calculated

Property Tax = Assessed Value × Mill Rate (Tax Rate) Example: A home assessed at $325,000 with a 1.2% tax rate = $3,900 per year. Assessed value is often a percentage of market value, which varies by state. |

3. What Can Make Your Property Taxes Go Down?

Many homeowners pay more than they need to. Here are legitimate ways your property tax bill can decrease:

Appealing Your Assessment

If your home’s assessed value seems too high, you have the legal right to appeal. Gather evidence such as recent sale prices of comparable homes in your area, a professional appraisal, or documentation of property damage. Appeals are handled at the local government level, and a successful appeal can lower your assessed value—and your tax bill. [5]

Applying for Exemptions and Credits

Many states and counties offer programs that reduce property taxes for qualifying homeowners:

- Homestead Exemption: Reduces taxable value for your primary residence. Available in most states.

- Senior Citizen Exemption: Reduced rates for homeowners aged 65 and older.

- Disability Exemption: Tax relief for homeowners with qualifying disabilities.

- Veterans’ Exemption: Property tax reductions for U.S. military veterans.

- Agricultural Exemption: Lower assessments for farmland used for agricultural purposes.

Correcting Errors on Your Assessment

Assessment offices process thousands of properties and mistakes happen. If your record shows incorrect square footage, an extra bathroom, or a finished basement that is actually unfinished, correcting those errors can result in a lower assessment. Contact your assessor’s office and request a review.

Market Value Declines

If home values in your neighborhood decline, your assessed value may be adjusted downward at the next reassessment cycle. Monitor your property’s market value relative to your assessed value annually.

| 💡 Did You Know?

According to the Tax Foundation, median annual property tax bills range from approximately $900 in Alabama to over $9,000 in New Jersey. Knowing your state’s position helps you evaluate whether your bill is in line with local norms. [6] |

4. Understanding Form 1098: Real Estate Taxes Explained

Form 1098 is the Mortgage Interest Statement your lender sends by January 31 each year. While its primary purpose is to report mortgage interest, it also includes property tax information when your taxes are paid through escrow. [3]

Key boxes on Form 1098:

- Box 1: Total mortgage interest you paid during the year.

- Box 5: Mortgage insurance premiums paid.

- Box 10: Real estate taxes paid on your behalf through the escrow account.

The Box 10 figure is what you will use when claiming the property tax deduction on your federal return. It represents the same taxes levied by your local government—reported here under the IRS label “real estate taxes.”

Note on timing discrepancies: The amount on Form 1098 may occasionally differ slightly from your county tax bill. This can occur when your lender pays taxes on a schedule that does not align perfectly with the county billing cycle, or when supplemental assessments are issued mid-year. Always verify with your lender if you spot a significant difference.

5. How Real Estate Taxes Affect Your Federal Tax Return?

Real estate taxes are generally deductible on your federal income tax return as part of the State and Local Tax (SALT) deduction, subject to current law. [1]

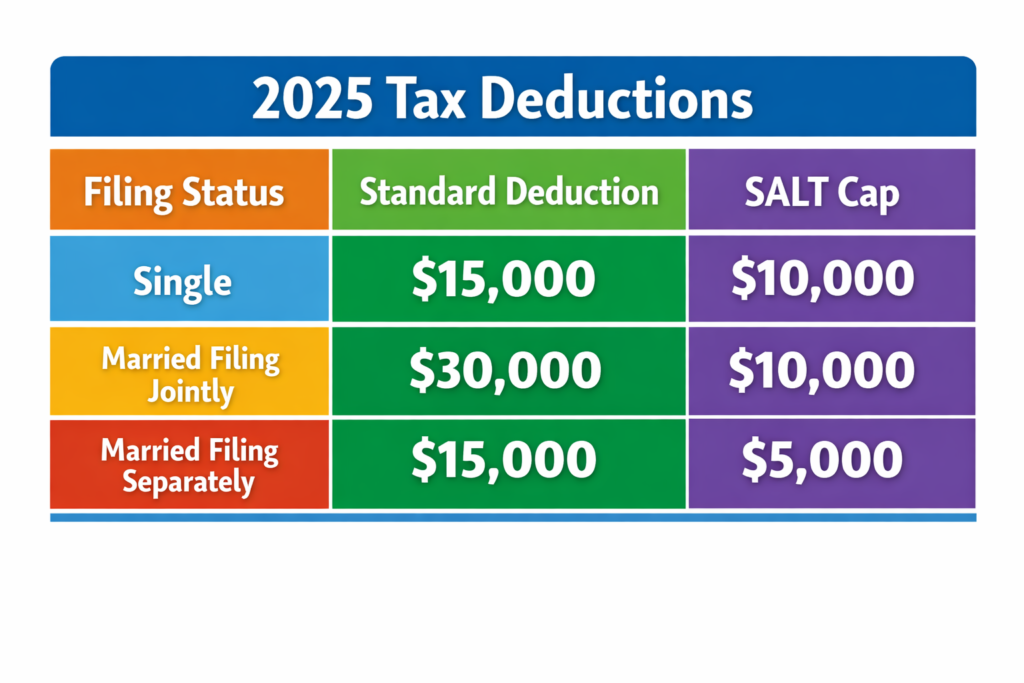

The SALT Deduction Cap

Under the Tax Cuts and Jobs Act of 2017, the total SALT deduction—which includes real estate taxes, state income taxes, and local taxes—is currently capped at $10,000 per return ($5,000 for married filing separately). This cap applies through at least 2025 under current law. Consult a qualified tax professional for the most current status.

2025 Standard Deduction and SALT Cap Reference:

Source: IRS Publication 530 [2]

How to Claim the Deduction

To deduct real estate taxes, you must:

- Itemize deductions using Schedule A (Form 1040).

- Have total itemized deductions that exceed your standard deduction.

- Have paid the taxes during the tax year in question (either directly or through escrow).

What You Cannot Deduct

According to IRS Publication 530, the following property-related charges are not deductible as real estate taxes: [2]

- Transfer taxes or stamp taxes paid when purchasing property

- Homeowners association (HOA) fees

- Service charges for trash, sewer, or water

- Assessments for local improvements that increase property value (such as new sidewalks or drainage systems)—though these may be added to your cost basis

Why are the premiums for homeowners insurance more expensive than those of renters insurance?USA

6. Real Estate Taxes and Your Mortgage Escrow Account

Most mortgage lenders require homeowners—especially those who put down less than 20%—to maintain an escrow account. This account collects a portion of your monthly payment and holds the funds until property taxes and homeowners insurance premiums are due. [4]

How the PITI Payment Works

Your monthly mortgage payment is often referred to as “PITI,” which stands for:

- P – Principal: The portion that reduces your loan balance.

- I – Interest: The lender’s fee for the loan.

- T – Taxes: Your estimated real estate taxes, collected monthly.

- I – Insurance: Homeowners insurance premiums (and mortgage insurance if applicable).

Annual Escrow Review

Federal law requires your mortgage servicer to conduct an annual escrow analysis to confirm that the collected amount covers anticipated taxes and insurance. If taxes rise, your monthly payment may increase. If taxes fall or a surplus has built up, you may receive a refund or see a payment reduction. [4]

| ⚠️ Escrow Shortage Tip

If your lender identifies an escrow shortage, they are required by federal law (RESPA) to notify you and offer a repayment plan. You can pay the shortage in a lump sum or spread it over 12 months. Contact your servicer promptly if you receive an escrow shortage notice. |

7. Are County Taxes the Same as Real Estate Taxes?

When people ask about “county taxes” in a homeownership context, they are generally referring to the real estate tax portion of their property tax bill. However, your total property tax bill is usually composed of several levies from different jurisdictions.

A typical property tax bill might break down as follows:

- County general fund

- Local school district

- City or municipality

- Special districts (fire, water, flood control)

For example, a $5,200 annual property tax bill might include $1,500 for the county, $2,600 for the school district, $800 for city services, and $300 for a special fire protection district. The sum of all these is your total real estate tax or property tax for the year.

Counties may also levy other taxes separately—such as personal property taxes or county income taxes—but in everyday homeownership conversation, “county taxes” almost always refers to the real estate portion.

8. The Connection Between Property Insurance and Property Taxes

While homeowners insurance and property taxes are separate obligations, they are closely connected in practice:

- Escrow bundling: Most lenders collect both insurance premiums and property taxes through the same escrow account, ensuring neither is missed.

- Lender requirements: Lenders require proof of homeowners insurance as a condition of your mortgage. They also monitor property tax payments because unpaid taxes can result in tax liens that threaten their collateral.

- Community protections: Property taxes fund local fire departments and emergency services—the same services that reduce your insurance risk and can influence your premium rates.

- Tax deductibility differences: Real estate taxes are deductible (subject to the SALT cap). Homeowners insurance premiums on a primary residence generally are not, unless part of your home is used for business.

9. Key Takeaways for U.S. Homeowners

- Real estate taxes and property taxes are the samein most homeownership contexts.

- Form 1098, Box 10reports the real estate taxes your lender paid through escrow.

- The SALT deductionallows you to deduct real estate taxes, capped at $10,000 combined with other state and local taxes.

- You can reduce your property taxthrough exemptions, successful appeals, and correcting assessment errors.

- Your monthly mortgage payment(PITI) typically includes property taxes collected in escrow.

- County taxesgenerally refer to the county portion of your property tax bill, which may include several separate levies.

- Keep thorough records—Form 1098, tax bills, and receipts—for at least three years after filing your tax return.

| 📌 Disclaimer

This article is for general informational purposes only and does not constitute legal or tax advice. Tax laws change. Always consult a licensed CPA, enrolled agent, or tax attorney for guidance specific to your situation. |

References & Citations

All information in this article is drawn from or verified against official U.S. government and nonpartisan sources. The following sources were consulted in preparing this guide:

| # | Source | URL | Description |

| 1 | IRS — Topic No. 503: Deductible Taxes | https://www.irs.gov/taxtopics/tc503 | Official IRS guidance on deductible taxes, including real estate and property taxes. |

| 2 | IRS Publication 530 — Tax Information for Homeowners | https://www.irs.gov/forms-pubs/about-publication-530 | IRS guide covering what homeowners can and cannot deduct, including real estate taxes. |

| 3 | IRS — Understanding Your Form 1098 | https://www.irs.gov/forms-pubs/about-form-1098 | Official explanation of Form 1098, including Box 10 real estate taxes reported by mortgage lenders. |

| 4 | Consumer Financial Protection Bureau (CFPB) — Escrow Accounts | https://www.consumerfinance.gov/ask-cfpb/what-is-an-escrow-or-impound-account-en-140/ | Federal consumer protection guidance on how mortgage escrow accounts work for taxes and insurance. |

| 5 | USA.gov — Property Taxes | https://www.usa.gov/property-taxes | Government overview of how property taxes are assessed, collected, and appealed across the United States. |

| 6 | Tax Foundation — Property Taxes by State | https://taxfoundation.org/data/all/state/property-taxes-by-state-county/ | Nonpartisan research on median property tax rates and bills across all U.S. states. |

| 7 | HUD — Homebuyer’s Guide to Taxes | https://www.hud.gov/topics/buying_a_home | U.S. Department of Housing and Urban Development resource for understanding homeownership costs, including taxes. |

© 2025 InsuranceInfoUSA.com — All rights reserved. Content may not be reproduced without permission.