Cheap Business Insurance for Contractors USA 2026: Your Complete Guide to Staying Protected Without Breaking the Bank

Introduction

Listen, I get it. You’re running a contracting business, and every dollar counts. The last thing you want is to pay thousands of dollars a year for insurance that feels like dead money—until you actually need it. Then suddenly, that “expensive” policy becomes the best investment you ever made.

Here’s the reality in 2026: you don’t have to choose between affohttps://hix.ai/?ref=nwzjmgjrdable and adequate coverage. The insurance market for contractors has evolved dramatically over the past few years. Digital-first companies, streamlined underwriting, and increased competition mean you have legitimate options to get solid protection without feeling like you’re financing an insurance executive’s yacht.

But here’s what most contractors get wrong: they either skip insurance entirely (yikes—one lawsuit wipes you out), or they overpay because they don’t know what to compare or how to negotiate. This guide cuts through the noise and gives you exactly what you need to make an informed decision in 2026.

We’re covering 10+ real insurance options, explaining what actually matters, sharing money-saving tactics that actually work, and helping you understand why this stuff matters beyond just “it’s the law.” By the time you finish reading, you’ll know exactly which direction to move and what questions to ask.

Let’s do this.

Understanding Contractor Insurance Basics

Why you actually need contractor insurance (and it’s not just legal)?

Here’s the uncomfortable truth: one accident, one injury on your jobsite, or one unhappy client can end your business. I’m not being dramatic—I’m being honest.

A homeowner slips on your wet concrete and breaks their leg. That’s easily $50,000+ in medical bills and lost wages, and they’re looking at you to cover it. Or a subcontractor gets hurt and claims you didn’t provide a safe workplace. Or your work causes $100,000 in damage to a client’s property. Without insurance, these aren’t abstract risks—they’re your personal financial responsibility, and they can bankrupt you in court.

Insurance isn’t just a legal checkbox (though in many cases, it is required). It’s your business’s safety net. When things go wrong—and in contracting, things sometimes do—insurance means the difference between a manageable claim and losing everything you’ve built.

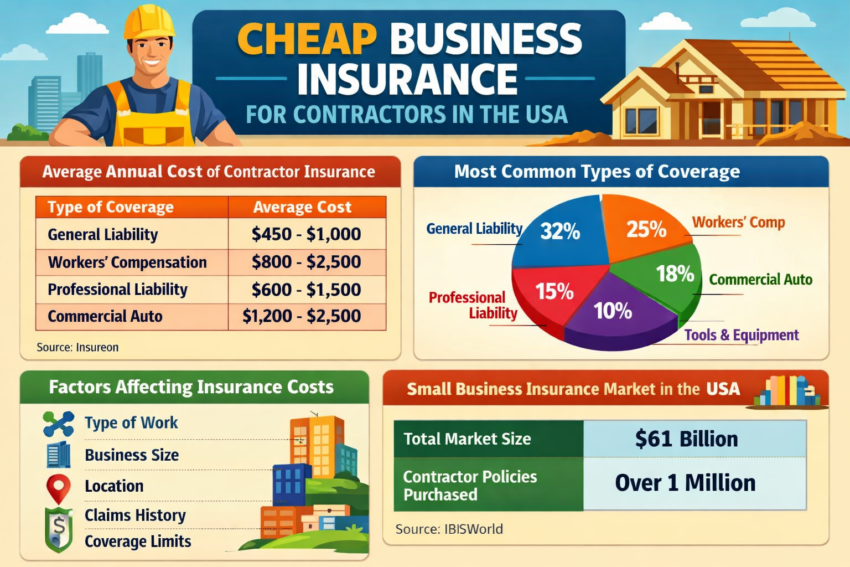

The four coverage types you need to know about

General Liability Insurance (GL) is the foundation. It covers bodily injury, property damage, and advertising injury caused by your work. If you knock over a client’s lamp while working in their home, GL covers it. If a client gets hurt and blames your work, GL covers the legal defense and damages.

Workers’ Compensation Insurance (required in most states if you have employees) covers medical costs and lost wages when your employees get injured on the job. Even if you’re a solo operator planning to stay solo, understanding this matters because some clients require proof you have it before they’ll hire you.

Commercial Auto Insurance covers vehicles you use for business purposes. Your personal auto policy explicitly does not cover business use—this is a massive gap most contractors don’t realize until they need it.

Tools & Equipment Insurance (also called inland marine or equipment floater) covers your expensive tools and equipment against theft, damage, or loss. When you’ve got $15,000+ in tools, this becomes pretty important.

Most contractors need at least GL and Workers’ Comp. Many need all four.

How much coverage you actually need?

The honest answer: it depends on your specific situation, but there’s a formula that helps.

Look at your largest project value. Most contractors should carry at least $1 million in General Liability coverage. Some clients—especially larger commercial or government projects—require $2 million or more. If you’re doing high-value work, aim higher. If you’re doing smaller residential jobs, $1 million is usually the baseline that keeps most doors open.

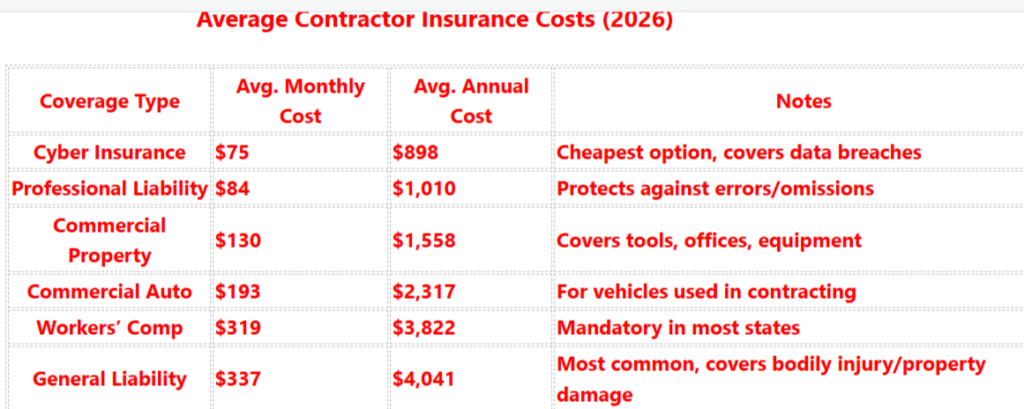

Average Contractor Insurance Costs (2026)

For Workers’ Compensation, your state mandates minimums based on your payroll. There’s no “choosing” here—you either meet the requirement or you’re breaking the law.

Equipment coverage should at least match your tool inventory value. If you’ve got $20,000 in tools, insure them for $20,000.

The key insight: don’t guess. When you’re getting quotes, ask each company what coverage limit they typically recommend for your trade and project types. They’ve seen thousands of claims and can give you real guidance.

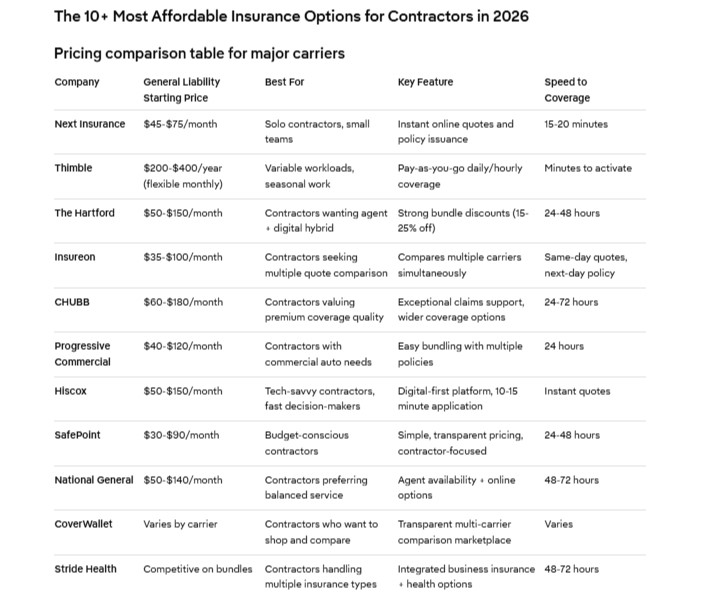

The 10+ Cheap Business Insurance Options for Contractors in 2026

1. Next Insurance

What it is? An online-first platform designed specifically for small contractors and service businesses.

What you’ll pay: Starting around $45-75/month for General Liability coverage for solo contractors, depending on your trade and location. Workers’ Comp and bundled packages run higher, but the digital model keeps costs competitive.

Why it’s affordable: They’ve stripped out the middleman. No local insurance agent taking a commission, no unnecessary overhead—just a streamlined online application and instant quotes.

Best for: Solo contractors and small teams who are comfortable applying online without hand-holding from an agent.

What makes it real:

- Fast online application (often 15-20 minutes)

- Instant policy availability

- Transparent pricing with no surprises

- Can adjust coverage as your business grows

Consideration: Some contractors prefer talking to an actual person, and Next Insurance is purely digital. If you’re someone who needs to chat with an agent, this might feel impersonal.

2. Thimble

What it is? The gig-economy insurance company. They pioneered short-term, flexible coverage for contractors.

What you’ll pay: Hourly or daily policies starting at just a few dollars per day. A full year of General Liability runs around $200-400 for many solo contractors, making it incredibly cheap.

Why it’s affordable: You only pay for coverage when you need it. Taking a month off? You’re not paying. Working five jobs a week? Scale up easily.

Best for: Contractors with variable workloads, seasonal work, or those just starting out who don’t want to commit to annual premiums.

What makes it real:

- Flexible monthly plans

- Add coverage on the fly

- Great for testing out insurance before committing to annual policies

- Mobile app makes everything accessible

Consideration: Some clients may want you to have traditional annual policies (which shows long-term commitment), and Thimble’s short-term model might not satisfy them. Also, paying monthly can add up to more than annual rates.

3. The Hartford

What it is? A legacy insurance company that’s adapted well to the contractor market in 2026. They’ve got serious financial backing and decades of claims-handling experience.

What you’ll pay: Generally $50-150/month for GL depending on your specific trade, location, and project types. Workers’ Comp and bundles run higher but include better discounts.

Why it’s affordable: They offer substantial multi-policy discounts. Bundle GL, Workers’ Comp, and tools coverage, and you’re looking at real savings compared to buying separately.

Best for: Contractors who want a hybrid approach—digital application but with the option to talk to an actual agent when needed.

What makes it real:

- Can apply online but also work with local agents

- Strong financial ratings and fast claims processing

- Good discount structure for bundled policies

- Available in all 50 states

Consideration: Their pricing isn’t the absolute cheapest when you compare single GL policies, but the bundle discounts and service quality often make it the better overall value.

4. Insureon

What it is? Another online platform specifically built for contractors and small service businesses, with a strong focus on making complex insurance simple.

What you’ll pay: Starting around $35-100/month for GL, depending on your trade. They’re competitive on pricing and offer bundled options.

Why it’s affordable: Automated underwriting means faster approvals and lower overhead costs that get passed to you.

Best for: Contractors who want a middle ground—online convenience but with easy access to chat support when needed.

What makes it real:

- Instant quotes for multiple carriers (they compare options for you)

- 24/7 customer support via chat

- Fast policy issuance

- Can get quotes same-day, policy by tomorrow

Consideration: Because they work with multiple carriers, your actual policy might come from different companies, so customer service experience might vary slightly.

5. CHUBB (ACE Group)

What it is? A premium insurance company known for excellent coverage but also increasingly competitive pricing for small contractors.

What you’ll pay: $60-180/month for GL, varying by trade. Generally mid-range pricing with excellent coverage quality.

Why it’s affordable: They’ve expanded aggressively into the small contractor market. While not the absolute cheapest, their bundled rates and claims reputation make them competitive.

Best for: Contractors who want premium coverage quality without premium prices, especially if you’re willing to bundle multiple policies.

What makes it real:

- Exceptional claims support (they’re known for paying claims quickly)

- Good coverage options including niche protections

- Available in all states

- Works with brokers if you prefer personal service

Consideration: You might pay slightly more than the absolute cheapest options, but you’re getting notably better service and coverage terms.

6. Progressive Commercial

What it is? The online insurance giant’s commercial division, offering policies designed for small business contractors.

What you’ll pay: Highly variable depending on trade and location, but often competitive at $40-120/month for GL. Known for offering discounts to bundlers.

Why it’s affordable: Progressive’s scale and automated systems mean competitive pricing. Their quote system is fast and transparent.

Best for: Contractors familiar with Progressive for personal insurance who want to consolidate. Also good if you have commercial auto needs.

What makes it real:

- Fast online quotes

- Easy policy management through their app

- Substantial discounts for bundling multiple policies

- Strong roadside assistance if you need commercial auto

Consideration: Coverage varies significantly by state, and some states have more options than others. Always confirm they operate in your specific area with your specific trade.

7. Hiscox

What it is? A London-based insurance company with serious digital chops and a growing presence in the U.S. contractor market.

What you’ll pay: Starting around $50-150/month for GL, depending on your specific situation.

Why it’s affordable: They use data and algorithms aggressively to underwrite and price policies, which keeps costs down compared to more traditional evaluation methods.

Best for: Tech-savvy contractors comfortable with a fully digital experience who want competitive pricing and good coverage terms.

What makes it real:

- Fully online application (usually takes 10-15 minutes)

- Instant quotes

- Can renew entirely online

- International company with solid financial backing

Consideration: Because they’re newer to the U.S. market, some contractors prefer more established companies. But their ratings and claims reputation are solid.

Cheapest Health Insurance for a Small Business with One Employee USA (2026 Guide)

8. SafePoint

What it is? A newer digital-first platform focused on contractors and trades.

What you’ll pay: Starting around $30-90/month depending on trade and coverage levels.

Why it’s affordable: They focus specifically on contractors, so they’ve built their systems around your actual needs rather than being a general business insurance company.

Best for: Contractors who want straightforward, no-frills coverage at competitive prices.

What makes it real:

- Simple, transparent pricing

- Quick online setup

- Contractor-specific coverage options

- Can adjust coverage mid-year if needed

Consideration: Smaller company means less brand recognition, though their ratings are solid. If brand recognition matters to your clients, this might matter.

9. National General

What it is: A long-established insurance company with solid presence across contractor categories.

What you’ll pay: $50-140/month for GL, varying by trade. Generally mid-range pricing.

Why it’s affordable: Wide network of agents and online options means competitive pricing. Often offers good rates for bundled policies.

Best for: Contractors who want a balance between online convenience and ability to work with local agents.

What makes it real:

- Available through agents or online

- Bundled discounts that actually add up

- Good in most states

- Responsive customer service

Consideration: Not the absolute cheapest option, but very reliable and solid middle-of-the-road pricing with good service.

10. CoverWallet

What it is? A platform that lets you compare and purchase insurance from multiple carriers in one place, like an insurance marketplace.

What you’ll pay: Highly variable since they work with multiple companies, but you get transparent comparison shopping.

Why it’s affordable: You literally see multiple quotes side-by-side and pick the best value. Competition between carriers means better pricing.

Best for: Contractors who want to compare options without calling 10 different companies.

What makes it real:

- Compare multiple quotes simultaneously

- See all coverage options clearly

- Can apply directly or work with their team

- Available in all 50 states

Consideration: More of a shopping platform than a direct insurer, so the experience depends partly on which carrier you choose. But the comparison aspect is genuinely valuable.

11. Stride Health (Bonus Option)

What it is? Primarily known for health insurance, but increasingly offering small business commercial coverage packages.

What you’ll pay: Competitive on bundled packages; not always the cheapest on GL alone, but strong value when bundling multiple policies.

Why it’s affordable: They focus on transparent pricing and helping small business owners actually understand what they’re buying.

Best for: Contractors who want to handle business insurance, health insurance, and potentially retirement planning through one integrated platform.

What makes it real:

- Integrated approach to business coverage

- Strong support team for questions

- Transparent about what each coverage actually covers

- Growing in availability

Consideration: Newer to the contractor insurance space, so less track record than some competitors.

Expert Money-Saving Tactics That Actually Work

Bundle policies for real discounts

Here’s what insurance companies don’t advertise loudly: bundling policies typically saves you 15-25% compared to buying separately. Get GL, Workers’ Comp, and Commercial Auto with the same company, and you’re looking at meaningful savings.

Call your quotes and ask: “What’s my total cost if I bundle everything?” Then compare that bundled price to what you’d pay piecing it together. The difference is often significant enough to justify choosing a slightly pricier single option if their bundle is cheaper overall.

Safety training and certifications reduce what you pay?

Here’s an easy one: take OSHA (Occupational Safety and Health Administration) training courses and get certified. Many insurance companies offer 5-15% discounts just for having safety certifications.

Why? Because they pay fewer claims on contractors with safety training. It’s that simple. A 10% discount on a $1,200 annual policy is $120 back in your pocket, and the training often takes just a few hours.

Strategic deductible choices

A deductible is what you pay out-of-pocket before insurance kicks in. Higher deductible = lower premium. Lower deductible = higher premium.

Here’s the strategy: set your deductible at what you can actually afford to pay if something happens. If you’ve got $10,000 in the bank and can handle that loss, a $10,000 deductible saves you money on premiums. If you’d be stressed about paying $5,000 out-of-pocket, choose a $1,000 deductible.

This isn’t about being cheap—it’s about matching your coverage to your actual financial situation.

Negotiate and ask for discounts explicitly

Insurance companies have flexibility. They won’t mention it, but if you ask, you’ll often get:

- Loyalty discounts if you stay with them for multiple years

- Early-payment discounts if you pay your annual premium upfront instead of monthly

- Multi-policy discounts (we covered this above)

- Claims-free discounts if you haven’t had any claims in several years

- Equipment/loss prevention discounts if you use certain safety equipment

When you’re getting quotes, literally ask: “Are there any other discounts I qualify for?” You’d be surprised.

Seasonal adjustments if your work varies

If you do heavier work in certain seasons, some companies allow you to adjust your coverage level and costs seasonally. You’re paying for more coverage during busy season, less during slow season. It takes communication with your insurance provider, but it can genuinely save money if your workload fluctuates significantly.

How to Get Your Quote and Move Forward?

What information you’ll actually need

When you’re ready to get quotes, have this information ready:

- Your trade/business type (even general contractors break down into specific categories)

- Annual revenue (approximate is fine)

- Number of employees (even if it’s zero)

- Types of projects you typically do (residential, commercial, both)

- Average project value

- Your location (state and general area)

- Loss history (any claims or incidents in the past 5-10 years)

Most online quotes take 15-30 minutes with this information ready. Don’t guess—be as accurate as you can.

Red flags to avoid

Prices that seem impossibly cheap – If a quote is 50% less than everyone else, dig into why. Sometimes it’s legitimate (great customer, clean record). Sometimes it’s because they’re excluding coverage you think you have.

Pressure to decide immediately – Good insurance companies want you to think about it. If someone’s pushing you to buy today, pause.

Vague coverage descriptions – You should understand exactly what’s covered and what’s not. If an agent can’t explain it clearly, move on.

Companies without solid ratings – Check AM Best ratings (the insurance industry standard). You want at least an “A” rating. Anything lower than that means there’s genuine financial risk that they can’t pay claims.

Key Takeaways: Your Action Plan

What you need to remember

- You need contractor insurance. One lawsuit or accident unravels everything you’ve built without it.

- Affordable coverage exists. You don’t choose between cheap and adequate—you can have both by shopping smart.

- Bundling saves real money. Get multiple policies from the same company and save 15-25%.

- $1 million in General Liability is the baseline. This is what most clients expect and what protects you from catastrophic claims.

- Workers’ Comp is non-negotiable if you have employees. You can’t operate legally without it, and one injury claim shows exactly why.

References

- Insureon. (2026). Average cost of contractor insurance in the U.S. Retrieved from https://www.insureon.com

- IBISWorld. (2026). Small Business Insurance Market Size & Industry Statistics in the U.S. Retrieved from https://www.ibisworld.com

- The Hartford. (2026). Contractor business insurance cost and coverage guide. Retrieved from https://www.thehartford.com

- Progressive Commercial. (2026). Business insurance for contractors: Coverage and pricing. Retrieved from https://www.progressivecommercial.com

- U.S. Small Business Administration (SBA). (2026). Small business insurance requirements and resources. Retrieved from https://www.sba.gov

- National Association of Insurance Commissioners (NAIC). (2026). Insurance cost trends and regulatory data. Retrieved from https://www.naic.org

- U.S. Bureau of Labor Statistics (BLS). (2026). Occupational injury and insurance cost data for contractors. Retrieved from https://www.bls.gov

Humera Khan is a professional digital content creator, SEO strategist, and data researcher specializing in the U.S. insurance market. Formally trained in advanced Content Writing, Search Engine Optimization, and Digital Marketing through the DigiSkills.pk program—executed by the Virtual University of Pakistan—Humera applies precise analytical standards to complex financial and corporate policy data. Her core mission for InsuranceInfoUSA is to provide readers with highly credible, transparent, and accessible insurance guidance. To maintain the highest level of factual integrity, her research methodology relies strictly on authoritative, verified industry benchmarks, with complete primary source citations included at the end of every guide to ensure total transparency and data reliability.To ensure total transparency and data reliability. For editorial inquiries or direct questions, she can be reached at Contact@insuranceinfousa.com.