How to Lower Car Insurance in the USA in 2026: A Real Person’s Guide to Saving Big

That insurance bill landing in your inbox every month? Yeah, I feel that. For pretty much all of us, car insurance is one of those expenses that just keeps climbing, and it seems impossible to escape.

But here’s the thing—and this actually surprised me when I found out—you have way more control over what you’re paying than you probably realize. The insurance industry isn’t some mysterious black box. In 2026, there are real, practical strategies that actually work: new technology, changing how insurance companies operate, and smart moves you can make starting today.

Now, I could tell you to “just shop around” and move on. That’s part of the answer, sure. But I want to walk you through the moves that genuinely move the needle. We’re talking about the new discount programs insurers are pushing right now, the coverage tricks most people miss, and the behavioral changes that can actually put hundreds back in your pocket.

Source: Progressive Insurance, 2025 Auto Insurance Pricing Data

Note: Data reflects liability-only policies with one vehicle and one driver.

Why Your Insurance Bill Keeps Going Up? (And It’s Not Just You)

Before we jump into fixing it, let’s talk about what’s actually happening behind the scenes. Once you understand why rates are climbing, the solutions make way more sense.

The real reasons your rates are rising

So your insurance isn’t going up just because. Between 2020 and 2024, the National Association of Insurance Commissioners reported that insurance premiums jumped by 25-30% across the country—and some states got hit even harder. There are a few solid reasons for this:

First up: repair costs have gotten crazy. Today’s cars are packed with electronics, sensors, and expensive materials. That fender bender that used to run $1,000? Now it’s $3,000 or more. Insurers are passing that straight to you.

Second: there are more accidents happening. More cars on the road, more people distracted by their phones, heavier traffic—insurers are paying out way more claims than they were five years ago. When their payouts go up, so do your premiums.

And third, there’s just inflation. Labor costs, parts prices, medical bills for injuries—everything your insurer deals with costs more. They need to keep their profit margins steady, so they raise your rates.

Here’s what the data actually shows:

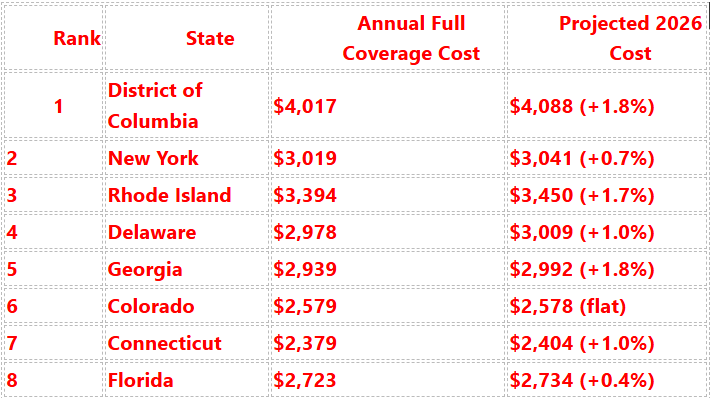

Most Expensive States for Car Insurance (2025-2026)

Source: Insurance Information Institute (III), 2022 State Data; Insurify 2025-2026 Projections

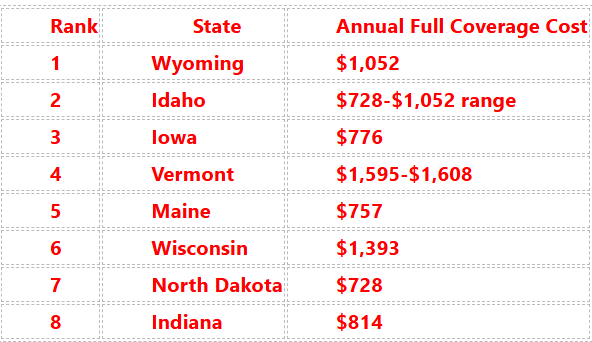

Least Expensive States for Car Insurance (2025-2026)

Source: Insurance Information Institute (III), National Association of Insurance Commissioners (NAIC) Database

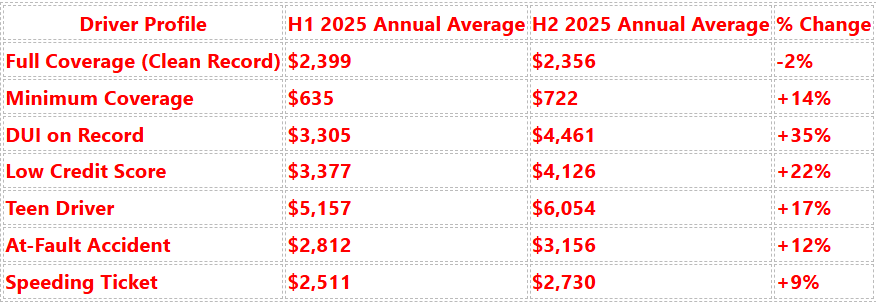

National Average Pricing Changes (2025-2026)

This critical data shows the widening gap between safe and high-risk drivers:

Source: AutoInsurance.com, 2026 Pricing Trends Report; Based on blended pricing estimates across major insurers for standardized driver profiles

Here’s what jumps out from that data: safe drivers with clean records are finally catching a break, while folks with accidents or tickets on their record are getting hit hard. That tells you something important—keeping a clean driving record genuinely matters.

Understanding why your car insurance keeps going up?

Historical Context: Between 2020-2024, average car insurance premiums increased by 25-30% nationally, with some states seeing even steeper increases.

Source: CNBC Select; National Highway Traffic Safety Administration (NHTSA); Bureau of Labor Statistics; Liberty Mutual Insurance Research

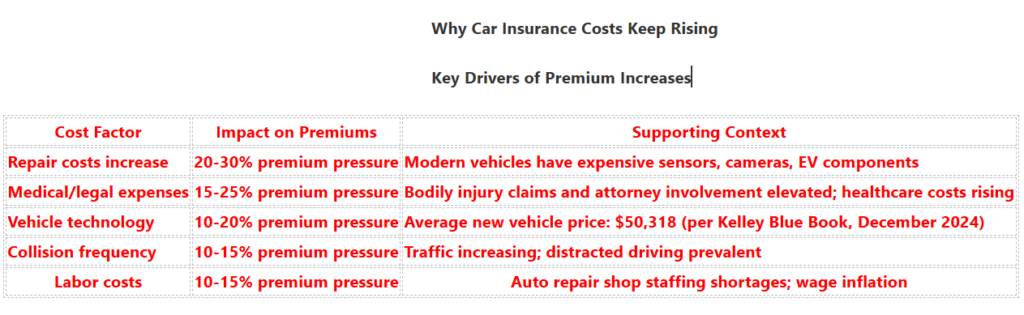

Before we jump into solutions, let’s talk about what’s actually driving those premium increases. Understanding this context makes the cost-cutting strategies way more powerful because you’ll know exactly where to apply pressure.

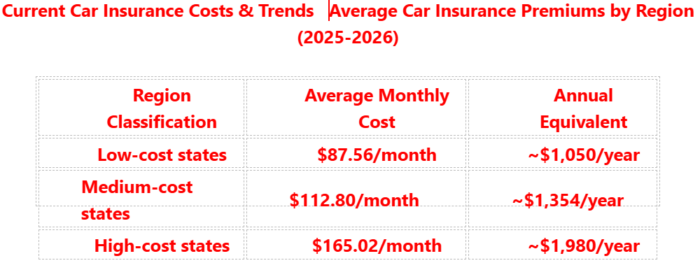

How much does car insurance cost in the USA 2026?

The inflation and claims cost reality

Your insurance rates aren’t rising just because your insurer feels like it. Between 2020 and 2024, the National Association of Insurance Commissioners (NAIC) reported that average car insurance premiums increased by approximately 25-30% across the country, with some states seeing even steeper jumps. The reasons? A few major factors are at play.

First, repair costs have skyrocketed. Modern cars contain sophisticated electronics, sensors, and lightweight materials that are expensive to repair. A fender bender that used to cost $1,000 might now run $3,000 or more. Insurers are passing these costs directly to consumers.

Second, there’s been a rise in collision claims. More cars on the road, more distracted driving, and increased traffic congestion mean insurers are paying out more claims than they did five years ago. When their payouts go up, premiums follow.

Third, inflation affects everything—labor costs, parts prices, medical expenses for injuries. Your insurer’s own operating costs have risen, and they need to maintain their profit margins.

The Discounts That Actually Work (And How to Get Them)

Okay, here’s the thing about insurance discounts: they’re everywhere. Insurers have them sitting there waiting for you to ask. Most people just… don’t ask. Let me walk you through what’s actually available right now.

Safe driving programs—these are genuinely worth it

Have you heard of usage-based insurance? It sounds fancy, but it’s pretty straightforward. You let the insurance company track your actual driving—usually through an app on your phone or a tiny device plugged into your car. Companies like State Farm, Progressive, Allstate, and Geico all offer this (they call them Drivewise, InsuRide, Snapshot, and DriveEasy).

Here’s what matters: good drivers can save 10-30% with these programs, depending on your insurer and how you actually drive. The insurer isn’t guessing about your risk based on your age or where you live—they have real data showing you’re careful. You keep your speed reasonable, you don’t brake hard constantly, you’re not texting and driving. That’s powerful.

Low mileage discounts—an easy win if it applies to you

Working from home? Carpooling? Just not driving much? Your insurer will usually knock 5-15% off your premium if you drive fewer than 7,500 to 10,000 miles per year. Some newer companies like Metromile actually specialize in this—you literally only pay for the miles you drive.

Bundling—it actually works

I know bundling gets talked about constantly, but it gets mentioned because it genuinely saves money. Combine your auto insurance with home, renters, or other policies, and you’ll typically get 15-25% off your auto policy alone. It’s one of the most reliable ways to save.

Loyalty matters too. Some insurers knock 5% or more off if you’ve been with them for three, five, or even ten years. Just ask—sometimes the savings are already there, and nobody’s told you about them.

Student discounts, professional discounts, and other wins

If you graduated recently, good news: many insurers still offer student discounts (usually 3-10% if your GPA is 3.0 or higher). And if you work in certain fields—engineering, healthcare, teaching, law—your employer might have group discounts negotiated with specific insurers. Worth checking.

Safety tech actually saves you money

If your car has automatic emergency braking, collision avoidance, blind spot monitoring, lane departure warning, or anti-theft devices, tell your insurer. These can knock 5-10% off what you’re paying.

Here’s what the major insurers are offering in 2026:

Top Insurance Companies & Discount Offerings (2026)

Source: Yahoo Finance 2026 Best Car Insurance Discounts Analysis; CNBC Select; Insurance Information Institute (III)

Restructuring Your Coverage (So You’re Not Overpaying or Underprotected)

This is where a lot of people mess up. They’re either paying for stuff they don’t need, or they’ve got deductibles so low they’re throwing away money every month.

Liability limits—don’t go cheap here

Your liability coverage is what protects the other person if you cause an accident. Here’s the critical part: liability is surprisingly affordable compared to the protection it gives you. But a lot of people are still running state-minimum coverage (usually $25,000-$50,000 in bodily injury). That’s… not a lot.

Serious accident? Medical bills, lost wages, pain and suffering—those numbers add up fast, and if they exceed your coverage, you’re personally responsible for the rest. That could mean wage garnishment or selling assets.

The smarter move? Bump up to $100,000/$300,000 if you can swing it. The extra premium is usually tiny—maybe $15-30 more per month—but your protection jumps way up. If you’ve got real assets, consider an umbrella policy on top.

Deductibles—the math needs to fit your life

Your deductible is what you pay out of pocket when you file a claim. Common ones are $250, $500, $1,000, or higher. The usual advice is “get the highest deductible you can afford,” but that needs some nuance.

If you’ve got an emergency fund and rarely file claims, jumping from a $250 to a $1,000 deductible might save you $300-500 per year. But if you’re living paycheck to paycheck, that $1,000 hit could be devastating. Be honest with yourself: can you actually afford to pay that deductible if you need to file a claim? If the answer is no, the savings aren’t worth the risk.

Dropping collision and comprehensive—sometimes it makes sense

Okay, this one’s controversial, but here’s the reality: if your car is older (think 10+ years old) and you’ve paid it off, the math might not favor keeping full coverage.

Quick example: your car’s worth $8,000, and you’re paying $150/month ($1,800/year) for collision and comprehensive with a $500 deductible. That’s nearly 23% of your car’s value every year. Run those numbers yourself—sometimes it actually makes more sense to self-insure and keep the money.

That said, if you still owe money on the car, your lender requires these coverages. So this option only applies if you own it outright.

The Actual Steps to Take This Week

Let’s move from theory to actual action. Here’s what you should do:

Step 1: Get real quotes

You should be shopping every 2-3 years, honestly. Use sites like Insurify or The Zebra, or just go straight to the insurers’ websites. Get 3-5 quotes with identical coverage so you’re genuinely comparing apples to apples.

One thing: online estimates are just estimates. Get actual bound quotes before you commit, and read the fine print. Some insurers price you differently based on credit score, so make sure you know what you’re being quoted on.

Step 2: Ask your current insurer about discounts

Call or chat with your insurer and ask straight up: “What discounts am I missing?” Have your policy open. Go through the list:

- Safe driving or low mileage programs

- Bundling with other policies

- Student or professional discounts

- Safety features in your car

- Paid-in-full discounts (paying upfront instead of monthly sometimes saves 5-10%)

- Claims-free discounts

Write down which ones you qualify for and ask exactly how much each saves you.

Step 3: Review your actual coverage

Pull up your policy declarations. Does your coverage actually match your situation? If you’ve paid off your car, reassess collision and comprehensive. If you have real assets, think about umbrella coverage.

Step 4: Let your driving record improve (it will)

This one takes time, but it matters: accidents and tickets fall off your record after 3-5 years depending on your state. Some insurers also offer accident forgiveness programs where your first accident doesn’t spike your rates.

Step 5: Actually switch if it makes sense

If you’ve been loyal for years and a competitor is quoting you 20%+ less for better coverage, switch. Your insurance company isn’t sentimental—they priced you based on their data. If someone else wants your business at a better rate, take it.

What’s Changing in Insurance Right Now? (2026)

Smaller, cheaper companies are making a move

Companies like Direct Line, Lemonade, and newer regional carriers are eating into the big guys’ market share. They operate with lower overhead—less office space, app-based customer service instead of phone lines—and pass those savings to you. If you’re comfortable handling everything through an app, these carriers can save you 10-20% compared to traditional insurers.

AI is pricing policies differently

Insurers are using AI and machine learning to price you more precisely based on actual risk data. This cuts both ways: if you’re genuinely low-risk, you might get a better rate. If your profile doesn’t fit traditional patterns, you might get flagged as high-risk. Shop around, especially if you’ve been told you’re a higher risk.

Pay-per-mile is becoming real

If you barely drive, services like Metromile or Root can be game-changers. You literally pay per mile—usually $0.15-0.25 per mile—plus a small monthly base. The catch: you need to be comfortable with GPS tracking and you really need to drive very little for this to make sense.

Real Numbers: What People Are Actually Saving

Let me put concrete numbers on this. Based on actual data from 2026:

- Average annual car insurance: $1,700-2,100 per year for a 35-year-old with a clean record and decent credit

- Bundling savings: 15-25% (that’s about $250-525/year)

- Usage-based insurance savings: 10-30% (roughly $170-630/year)

- Higher deductible (moving from $500 to $1,000): $200-400/year

- Shopping and switching: 15-40% (about $255-840/year)

Put a few of these together? A real person could save $500-1,500 annually. For a two-car household, we’re talking $1,000-3,000 per year. That’s significant money.

Here’s What You Should Actually Do

Look, you have real leverage here. Insurance rates aren’t locked in—these companies are fighting for your business, and the discounts are substantial if you know where to push.

Shop every 2-3 years minimum. Your insurer’s pricing changes, competitors emerge, your life situation shifts. Don’t stay just out of habit.

Use behavioral programs if you can. Usage-based insurance genuinely works if you drive safely. You could save $100-600 per year with minimal effort.

Audit your coverage. Make sure your deductibles and liability limits actually fit your real life and financial situation, not just what insurance companies default to.

Bundle and ask about discounts. One conversation with your insurer can net you $150-300 in annual savings if you’re not already getting them.

Don’t sacrifice actual protection to save money. It’s tempting to go with minimum liability, but coverage is cheap compared to the risk. Find the balance between affordability and real protection.

The bottom line? You’re almost certainly overpaying right now. It takes a couple hours to get quotes, call your insurer, and restructure your coverage. For savings that could hit $1,000+ per year, that’s a really solid return on your time.

Sources used in this guide:

- National Association of Insurance Commissioners (NAIC) — https://www.naic.org/

- Insurance Information Institute (III) — https://www.iii.org/

- Federal Trade Commission (FTC) Consumer Advice — https://consumer.ftc.gov/articles/0644-auto-insurance

- National Highway Traffic Safety Administration (NHTSA) — https://www.nhtsa.gov/

- IIHS (Insurance Institute for Highway Safety) — https://www.iihs.org/

- Consumer Reports — https://www.consumerreports.org/

- State Insurance Commissioner Offices — https://www.naic.org/state_web_services.htm

Note: Premium figures and discount percentages come from 2024-2025 insurance industry reports, state filings, and quote platform data. Your actual rates depend on location, driving record, vehicle type, age, and credit. Always get quotes from multiple insurers for your specific situation.

About the data: The insurance premium figures and discount percentages cited in this article are drawn from 2024-2025 insurance industry reports, state insurance commissioner filings, and aggregated pricing data from major insurance quote platforms. Individual rates vary significantly based on location, driving record, vehicle type, age, and credit score. Always obtain actual quotes from multiple insurers to compare real rates for your specific situation.

Humera Khan is a professional digital content creator, SEO strategist, and data researcher specializing in the U.S. insurance market. Formally trained in advanced Content Writing, Search Engine Optimization, and Digital Marketing through the DigiSkills.pk program—executed by the Virtual University of Pakistan—Humera applies precise analytical standards to complex financial and corporate policy data. Her core mission for InsuranceInfoUSA is to provide readers with highly credible, transparent, and accessible insurance guidance. To maintain the highest level of factual integrity, her research methodology relies strictly on authoritative, verified industry benchmarks, with complete primary source citations included at the end of every guide to ensure total transparency and data reliability.To ensure total transparency and data reliability. For editorial inquiries or direct questions, she can be reached at Contact@insuranceinfousa.com.