Average cost of health insurance USA (2026). If you live in the United States, health insurance isn’t just a financial decision — it’s a necessity. You want to know how much coverage will cost you each month, whether you’re buying through your employer, the Affordable Care Act (ACA) Marketplace, or directly from an insurer. In 2026, premiums have continued to rise modestly, but subsidies and employer contributions still make coverage accessible for most Americans.

This guide breaks down the average monthly and yearly costs, explains how family and individual plans differ, and shares expert insights to help you make smarter choices.

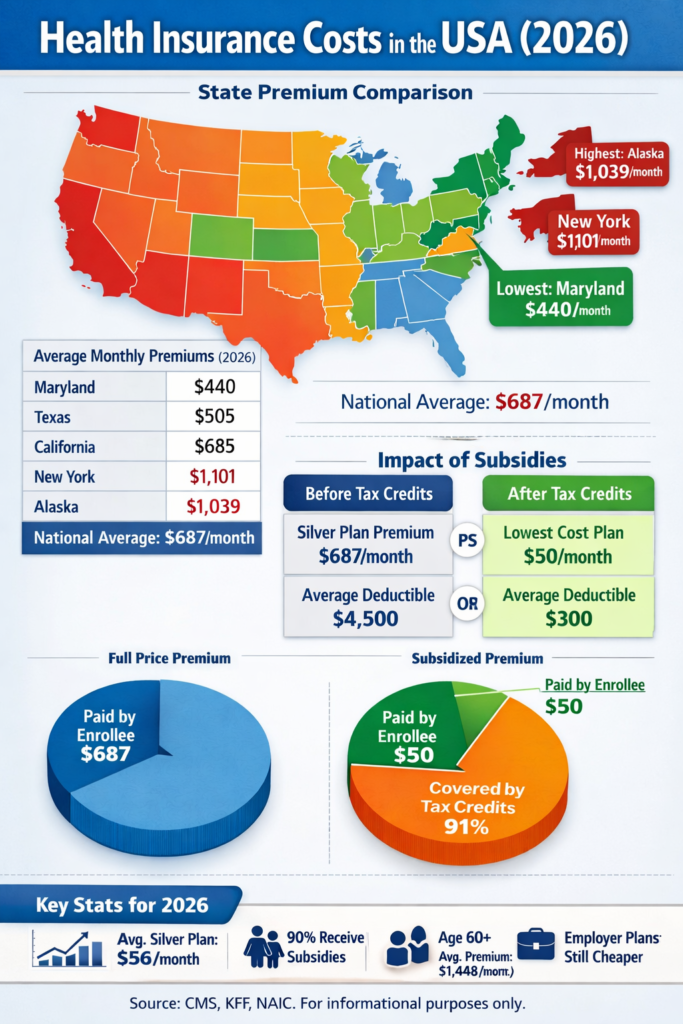

Average cost of health insurance USA per month

The average monthly premium for an adult on a Silver-tier plan in 2026 is around $687 before subsidies. However, most people pay far less after tax credits — sometimes as little as $50 per month for the lowest-cost plan.

Monthly premium breakdown by plan tier

| Plan Type | Average Monthly Premium (Pre‑Subsidy) | Coverage Level |

|---|---|---|

| Catastrophic | $290 | Very high deductible, limited to under‑30s |

| Bronze | $420 | Covers about 60% of medical costs |

| Silver | $560 | Benchmark plan, covers about 70% |

| Gold | $665 | Covers about 80% |

| Platinum | $780 | Covers about 90%, limited availability |

Factors that affect monthly premiums

- Age: Older adults pay up to three times more than younger enrollees.

- Location: State regulations and local healthcare costs influence pricing.

- Plan tier: Higher coverage levels mean higher premiums but lower deductibles.

- Income: Subsidies reduce costs for households earning up to 400% of the federal poverty level.

- Employer vs. marketplace: Employer plans often cost less because companies share the premium.

Common misconceptions

- “Cheaper plans always save money.” Bronze plans may look affordable, but high deductibles can lead to larger out‑of‑pocket expenses.

- “Employer insurance is always better.” Not always — some employers offer limited networks or high employee contributions.

- “Subsidies only apply to low‑income households.” Middle‑income families often qualify for partial credits under ACA rules.

- “Marketplace plans are low quality.” All ACA plans must meet federal standards for essential health benefits.

Expert tips

- Compare plans annually — premiums and networks change every year.

- Use the Healthcare.gov calculator to estimate your subsidy.

- Check state‑specific exchanges for local discounts.

- Consider Health Savings Accounts (HSAs) for tax advantages if you choose a high‑deductible plan.

Average cost of health insurance USA per year

Annual premium overview

When you multiply monthly premiums by 12, the numbers become more striking:

- Individual Silver plan: ~$8,244 per year

- Family plan (average): ~$22,000 per year (employer coverage)

- Employer contribution: ~$15,500 per year

- Employee share: ~$6,500 per year

These figures show how employer‑sponsored insurance remains the most common and cost‑effective option for many Americans.

Employer‑sponsored insurance trends

- Average family premium: ~$22,000 annually

- Deductibles: $4,500–$9,000 range

- Out‑of‑pocket maximums: $9,100–$18,200

- Employers increasingly shift costs to employees through higher deductibles and copays.

Year‑over‑year trends (2024–2026)

Premiums have grown about 3–5% annually, driven by inflation and increased healthcare utilization. Telehealth adoption and preventive care programs have helped slow the growth rate compared to pre‑pandemic years.

Expert insights

According to the Kaiser Family Foundation (KFF), premium stabilization in 2026 is largely due to extended ACA subsidies and improved insurer competition. The Centers for Medicare & Medicaid Services (CMS) also report that preventive care and virtual consultations are helping reduce long‑term costs.

Average health insurance cost USA family of 4

Family coverage breakdown

If you’re covering a family of four in the United States, health insurance is one of the largest household expenses. In 2026, the average monthly premium for family coverage is around $1,900, which equals $22,800 per year before subsidies.

- Employer‑sponsored insurance: Families typically pay about $6,500 annually, while employers contribute around $15,500.

- ACA Marketplace plans: Without subsidies, premiums average $1,900 per month, but tax credits can reduce costs dramatically.

- Private insurer plans: Families buying directly from insurers often face higher premiums (~$2,100/month) and fewer subsidy options.

Subsidy impact for families

Subsidies under the Affordable Care Act (ACA) are designed to make family coverage more affordable.

- Families earning up to 400% of the federal poverty level (FPL) qualify for tax credits.

- Example: A family of four earning $90,000 annually may pay around $350 per month after subsidies.

- On average, subsidies cover 91% of the lowest‑cost plan premium, making ACA Marketplace coverage accessible to middle‑income households.

State variations

Premiums vary widely depending on where you live:

- Cheapest states: Maryland (~$440/month), Utah (~$505/month), Colorado (~$520/month).

- Most expensive states: Alaska (~$1,039/month), New York (~$1,101/month), Vermont (~$980/month).

- The difference between the cheapest and most expensive states can exceed $600 per month.

📊 This is why comparing state‑specific exchanges and local insurer networks is critical for families.

Deductibles and out‑of‑pocket costs

Premiums are only part of the story. Families must also budget for deductibles and maximum out‑of‑pocket costs.

- Deductibles: $4,500–$9,000 range for family plans.

- Out‑of‑pocket maximums: $9,100–$18,200 depending on plan tier.

- Silver plans: Often balance affordability with moderate deductibles, making them the most popular choice for families.

Common misconceptions about family coverage

- “Employer insurance always covers everything.” In reality, many employer plans have high deductibles or limited provider networks.

- “Marketplace plans are only for low‑income families.” Middle‑income households often qualify for partial subsidies.

- “Family plans are cheaper per person.” While economies of scale exist, deductibles and out‑of‑pocket costs can still be high.

- “Gold plans are always better.” Gold plans reduce deductibles but may not be cost‑effective if your family rarely uses healthcare services.

Expert tips for families

- Compare Silver vs. Gold plans — Silver often balances premium cost and deductible size.

- Check Children’s Health Insurance Program (CHIP) eligibility for kids, which can reduce costs significantly.

- Review family vs. individual deductibles — some plans cap family costs more effectively.

- Consider telehealth‑inclusive plans for pediatric and routine care.

- Re‑evaluate coverage annually — premiums, subsidies, and provider networks change every year.

Key takeaway

For a family of four in 2026, the average health insurance premium is about $1,900 per month before subsidies, but most families pay far less thanks to ACA tax credits or employer contributions. The best strategy is to compare plans carefully, factor in deductibles, and use subsidies to minimize costs.