What is Covered in Fully Comprehensive Car Insurance?

Your Complete Guide (USA)

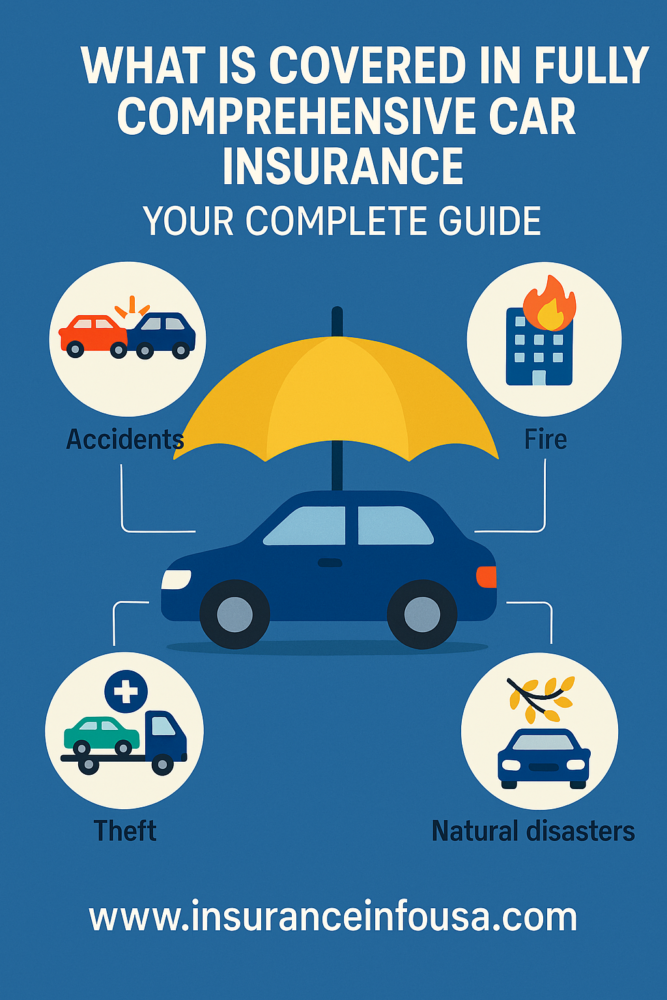

When shopping for car insurance in the United States, many drivers wonder: “What exactly does fully comprehensive coverage include?” Let’s break it down so you know what you’re paying for and why it matters.

Understanding Comprehensive Car Insurance

When people hear the word “comprehensive,” they often assume it means everything is covered. In reality, comprehensive insurance specifically protects against damages that occur outside of a collision. For example, if your car is stolen, vandalized, damaged in a hailstorm, or struck by a falling tree branch, comprehensive coverage steps in to pay for repairs or replacement.

It also covers wildlife encounters, such as hitting a deer, which can cause thousands of dollars in damage. What it does not cover are collision‑related accidents, medical bills, or personal belongings inside the car. Those require separate coverage types like collision insurance, personal injury protection (PIP), or renters/homeowners insurance.

The cost of comprehensive insurance varies depending on your car’s value, where you live, and your deductible choice. On average, U.S. drivers pay between $134 and $300 annually for this coverage.

Opting for a higher deductible can lower your monthly premium, but it means you’ll pay more out of pocket if you file a claim. Comprehensive insurance is particularly valuable for newer or high‑value cars, or for drivers living in areas prone to severe weather, high theft rates, or wildlife collisions. For older cars with low market value, however, the cost may outweigh the benefit.

Ultimately, comprehensive car insurance offers peace of mind. It ensures that when life throws unexpected challenges your way—whether it’s a storm, a thief, or a wandering deer—you won’t face the full financial burden alone. For many drivers, that security makes comprehensive coverage well worth the investment.

Sources

- Investopedia – Comprehensive Car Insurance: What It Covers and When to Buy (investopedia.com in Bing)

- MoneyGeek – Comprehensive Car Insurance Guide (moneygeek.com in Bing)

- Complete Guide 2025 – Comprehensive Car Insurance (ocho.com in Bing)

Comprehensive insurance covers:

- Complete vehicle theft

- Attempted theft that causes damage

- Vandalism (keyed paint, slashed tires, broken windows)

- Stolen car parts like catalytic converters

Weather‑Related Damage

Coverage includes damage from:

- Hailstorms

- Flooding

- Tornadoes and hurricanes

- Lightning strikes

- Falling tree branches

Animal Collisions and Wildlife Encounters

If you hit a deer or other wildlife, comprehensive insurance covers the damage. It also protects against rodent damage to wiring, bird strikes on windshields, and other wildlife‑related incidents.

Fire and Explosion Damage

Comprehensive insurance covers:

- Engine fires

- Electrical fires

- Arson

- Damage from nearby fires

Glass Damage and Windshield Replacement

Most policies include glass coverage, often with zero deductible in certain states, making windshield repair or replacement affordable.

Falling Objects

Coverage applies if your car is damaged by:

- Tree branches

- Rocks or debris

- Collapsing structures

Civil Disturbances and Riots

Comprehensive insurance covers damage caused during riots, protests, or civil unrest.

What Comprehensive Car Insurance Does Not Cover in USA?

| Covered by Comprehensive Insurance | Not Covered by Comprehensive Insurance |

|---|---|

| Theft of vehicle or car parts (e.g., catalytic converter) | Collision damage with another vehicle, guardrail, or building |

| Vandalism (keyed paint, broken windows, slashed tires) | Medical expenses for driver or passengers |

| Weather damage (hail, floods, tornadoes, hurricanes, lightning) | Liability for damage to other people’s property |

| Animal collisions (deer, moose, rodents chewing wiring) | Mechanical breakdowns, wear and tear, or engine failure |

| Fire and explosions (engine fires, arson, electrical fires) | Personal belongings stolen from inside the car (covered by home/renters insurance) |

| Falling objects (tree branches, rocks, debris, collapsing garage) | Intentional damage or illegal activity |

| Civil disturbances and riots | Custom modifications unless separately insured |

| Glass damage and windshield replacement | Rental car expenses unless rental reimbursement is added |

Collision Damage: If your car hits another vehicle, a guardrail, or a building, that falls under collision insurance, not comprehensive.

- Wear and Tear / Mechanical Breakdowns: Routine maintenance issues, worn tires, or engine failures are excluded. Comprehensive won’t pay for mechanical breakdowns or normal aging of your car.

- Intentional Damage or Illegal Activity: If you deliberately damage your own vehicle, commit fraud, or use your car in illegal activities, coverage is void.

- Racing or High‑Risk Activities: Damage sustained during organized racing, off‑road competitions, or reckless driving is excluded.

- Driving Under the Influence: Claims may be denied if the driver was intoxicated or impaired at the time of damage.

- Commercial Use (if policy is personal): Using your car for business purposes when insured under a personal policy can lead to claim denial.

- Geographic Limits: Some policies restrict coverage outside the U.S. or in specific regions.

- Personal Belongings Inside the Car: Stolen items like laptops or phones are covered under homeowners or renters insurance, not auto insurance.

✅ Key Takeaway

Comprehensive insurance is valuable for non‑collision risks like theft, vandalism, fire, weather, and animal strikes, but it does not cover accidents, wear and tear, or personal property. To build a complete safety net, drivers often combine comprehensive with collision coverage, liability insurance, and medical coverage (PIP or MedPay).

Sources

- Drive Smart Tools – What Not Covered by Comprehensive Car Insurance

- InsuredAndMore – What Does Comprehensive Insurance Not Cover?

- Car Bibles – What Comprehensive Car Insurance Does Not Cover

What is comprehensive deductible in car insurance in USA?

In the United States, a comprehensive deductible in car insurance is the fixed amount you agree to pay out of pocket before your insurance company covers the rest of a claim for non‑collision damage such as theft, vandalism, fire, weather events, or animal strikes.

For example, if your deductible is $500 and a hailstorm causes $3,000 worth of damage, you would pay $500 and your insurer would cover the remaining $2,500.

Deductibles are applied per incident, not annually, and typically range from $250 to $1,000, though some insurers may offer higher or lower options.

Choosing a higher deductible usually lowers your monthly premium but increases your financial responsibility when filing a claim, while a lower deductible raises your premium but reduces the upfront cost if damage occurs.

This balance between risk and affordability makes the deductible an important factor when customizing your car insurance policy.

Is Comprehensive Insurance Worth It?

It’s highly valuable if:

- Your car is financed or leased

- You own a newer or high‑value vehicle

- You live in a high‑theft area

- You reside in severe weather regions

- You drive in wildlife‑dense states

If your car’s value is very low, or you have strong emergency savings, you may reconsider.

Cost of Comprehensive Insurance

Average annual cost ranges from $100–$300, depending on your car, location, deductible, and driving history.

Tips for Getting the Best Coverage

- Shop around and compare quotes

- Bundle policies for discounts

- Maintain a clean driving record

- Ask about anti‑theft and safe driver discounts

- Review coverage annually

📚 Sources

- National Association of Insurance Commissioners (NAIC) – Auto Insurance Coverage (content.naic.org in Bing)

- FBI – Uniform Crime Reporting: Motor Vehicle Theft (fbi.gov in Bing)

- NOAA – Billion-Dollar Weather and Climate Disasters

- State Farm – Animal Collision Claims Report

- Insurance Information Institute – Auto Insurance Facts (iii.org in Bing)

- Experian – Comprehensive Car Insurance Coverage (experian.com in Bing)

- The Zebra – Average Cost of Car Insurance (thezebra.com in Bing)

- CNBC – Cheapest Car Insurance Companies (cnbc.com in Bing)

Humera Khan is a professional digital content creator, SEO strategist, and data researcher specializing in the U.S. insurance market. Formally trained in advanced Content Writing, Search Engine Optimization, and Digital Marketing through the DigiSkills.pk program—executed by the Virtual University of Pakistan—Humera applies precise analytical standards to complex financial and corporate policy data. Her core mission for InsuranceInfoUSA is to provide readers with highly credible, transparent, and accessible insurance guidance. To maintain the highest level of factual integrity, her research methodology relies strictly on authoritative, verified industry benchmarks, with complete primary source citations included at the end of every guide to ensure total transparency and data reliability.To ensure total transparency and data reliability. For editorial inquiries or direct questions, she can be reached at Contact@insuranceinfousa.com.