What Does Liability Insurance Cover for a Car USA? Guide. Liability insurance is the legal foundation of auto coverage in the United States.

It protects you financially when you cause harm to others, but it does not repair your own car. In 2026, with medical costs rising, expensive EV repairs, and evolving state laws, carrying only minimum coverage could leave your savings and wages at risk.

This guide explains what liability insurance covers, recent law changes, and how to choose the right limits for peace of mind.

What Does Liability Insurance Cover for a Car USA?

Bodily Injury Liability (BI)

Bodily injury liability pays for injuries you cause to other people in an accident. It covers:

- Hospital bills, surgery, and rehabilitation

- Lost wages if the injured person cannot work

- Pain and suffering settlements

- Funeral expenses in fatal crashes

- Legal defense costs if you are sued

Important: BI does not cover your own medical bills or those of your passengers. In 2026, the average emergency room visit exceeds $15,000, making state minimums inadequate.

Property Damage Liability (PD)

Property damage liability pays for damage to someone else’s property, including:

- Repairs or replacement of another driver’s car

- Damage to fences, guardrails, mailboxes, or buildings

Note: PD does not cover repairs to your own vehicle. EV collision repairs often exceed $20,000, surpassing old $10,000 PD minimums.

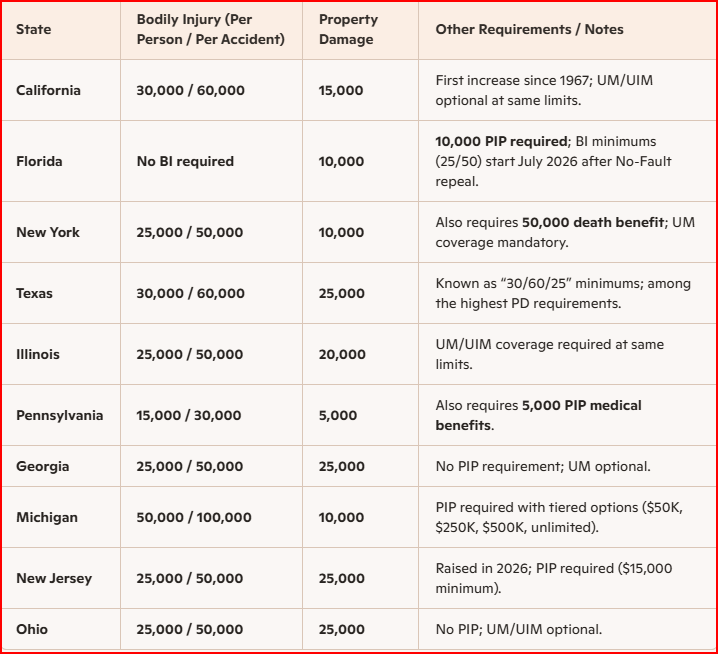

State Requirements and 2026 Law Changes

- California: Minimums increased to 30/60/15 effective January 2025.

- Florida: Scheduled repeal of “No‑Fault” PIP system in July 2026. Drivers must carry BI limits of 25/50.

- New Jersey: Minimums raised to 25/50 for bodily injury.

- Colorado: New transparency law requires insurers to disclose wildfire risk scores (signals stricter disclosure trends in auto).

States are raising limits due to inflation and “nuclear verdicts” (lawsuits exceeding $10M). A $15,000 cap from the 1980s cannot cover a modern ER visit.

How Split Limits Works?

Split limits divide liability insurance into three independent caps: per person injury, per accident injury, and property damage. While they provide clarity and customization, they can leave you financially vulnerable if you carry only state minimums. In 2026, experts recommend at least 100/300/100 coverage — or higher — to protect against rising medical and repair costs.

Example: 25/50/25

- $25,000 per person for bodily injury

- $50,000 total per accident for bodily injury

- $25,000 for property damage

Expert tip: In 2026, middle‑class households should consider 100/300/100 limits to avoid wage garnishment if claims exceed coverage.

Buyer’s Guide: Choosing the Right Limits

To choose the right auto insurance limits, you need to align coverage with your financial risk, vehicle value, and exposure to uninsured drivers. The safest strategy is to match liability coverage to your net worth, add UM/UIM protection, and consider an umbrella policy for extra peace of mind.

🔍 Step‑by‑Step Buyer’s Guide

1. Audit Your Assets

- Match Bodily Injury (BI) coverage to your net worth.

- If your net worth is $250,000, aim for liability limits of at least 250/500/100 ($250k per person, $500k per accident, $100k property damage).

- Homeowners should carry higher BI limits.

- Owning property increases your exposure to lawsuits; minimum state limits (like 25/50/25) are rarely sufficient.

2. Check Your Car’s Value

- Drop full coverage if your car is worth < $4,000.

- Collision and comprehensive premiums may exceed the payout value.

- Example: A 15‑year‑old sedan worth $3,500 → liability‑only coverage is more cost‑effective.

3. Add Uninsured/Underinsured Motorist (UM/UIM)

- 1 in 7 U.S. drivers is uninsured nationally; in some states, rates exceed 25%.

- UM coverage pays for your medical bills if hit by an uninsured driver.

- UIM coverage fills the gap when the at‑fault driver’s limits are too low.

- States vary: some mandate UM/UIM, others require written rejection.

4. Get Quotes from Top Carriers

- State Farm, Geico, Progressive, Lemonade, Root all offer liability‑only policies.

- Many provide telematics discounts (usage‑based programs that reward safe driving).

- Compare quotes online and through agents; premiums vary by ZIP code, age, and driving history.

5. Consider Umbrella Policies

- Umbrella insurance adds $1M+ liability protection for ~$150–$550/year.

- Standard umbrellas cover third‑party liability (when you’re at fault).

- Important caveat: Umbrellas usually do not cover UM/UIM unless you add an endorsement. Excess UM/UIM costs $75–$200 per million when available.

- Best for homeowners, high‑net‑worth individuals, or families with teen drivers.

📊 Comparison Table

| Coverage Type | Purpose | Typical Cost | Key Consideration |

|---|---|---|---|

| BI Liability | Pays others’ medical bills | Included in auto policy | Match to net worth |

| Property Damage Liability | Pays for others’ car/property | Included | Minimum $50k recommended |

| Collision/Comprehensive | Pays for your car | $300–$600/year | Drop if car < $4k |

| UM/UIM | Protects you from uninsured drivers | $50–$150/year | 1 in 7 drivers uninsured |

| Umbrella | Adds $1M+ liability | $150–$550/year | UM/UIM endorsement extra |

- Under‑insuring liability risks personal asset seizure in lawsuits.

- Skipping UM/UIM leaves you exposed to medical bills if hit by an uninsured driver.

- Dropping full coverage too early may cost you if your car is stolen or damaged.

- Umbrella gaps: Without UM/UIM endorsement, umbrellas only protect when you’re at fault.

✅ Action Plan:

- Calculate your net worth → set BI limits accordingly.

- Check your car’s market value → decide on full vs. liability‑only.

- Add UM/UIM to match liability limits.

- Compare quotes from multiple carriers with telematics discounts.

- Add umbrella coverage if you own property or have significant assets.

2026 Trends Reshaping Liability Insurance

In 2026, liability insurance is being reshaped by three major forces: AI-driven “touchless claims” that settle minor accidents in minutes, rising EV repair costs that strain traditional property damage limits, and the mainstream adoption of telematics, with 40% of U.S. drivers now using usage-based insurance. insurasales.com roadbuddy.ai spglobal.com

⚡ AI Claims Processing (“Touchless Claims”)

- AI-powered claims systems now use real-time analytics and vehicle sensor data to detect crashes and assess damage instantly.

- Minor accidents (e.g., fender benders) can be settled in minutes instead of weeks, reducing adjuster involvement and litigation.

- Machine learning models improve fraud detection and risk segmentation, lowering costs for insurers and speeding payouts for policyholders. insurasales.com

🚗 EV Repair Costs and Liability Limits

- EV repairs average 18% higher than gas-powered vehicles due to expensive batteries, proprietary electronics, and calibration needs. roadbuddy.ai

- A $25,000 property damage limit may not cover a totaled Tesla or other high-value EV.

- Battery replacement alone can exceed $15,000–$20,000, making higher liability limits (e.g., $50k–$100k PD) increasingly necessary.

- EV-specific insurance products now include battery degradation coverage and charging equipment protection, reflecting new risk categories. roadbuddy.ai

📡 Telematics (Usage-Based Insurance, UBI)

- 40% of U.S. drivers now participate in telematics programs, up from ~25% in 2023. insurasales.com

- Insurers track speed, braking, mileage, and time of day to personalize premiums.

- Safe drivers can save 10–30% annually, while risky driving increases rates.

- Longitudinal telematics data is also used to inform vehicle design improvements and personalized risk assessments at purchase. insurasales.com

📊 Comparison Table: 2026 Liability Insurance Trends

| Trend | Impact | Risk/Opportunity |

|---|---|---|

| AI Claims Processing | Faster settlements, reduced fraud | Lower admin costs, better customer satisfaction |

| EV Repair Costs | 18% higher than gas cars | $25k PD limit often insufficient |

| Telematics (UBI) | 40% adoption in U.S. | Personalized pricing, discounts for safe drivers |

⚠️ Risks & Trade-Offs

- AI claims may raise privacy concerns due to reliance on sensor and telematics data.

- EV repair inflation could make minimum liability limits obsolete, exposing drivers to lawsuits.

- Telematics adoption creates data-sharing risks; insurers must balance personalization with consumer trust.

✅ Key Takeaway: In 2026, liability insurance buyers should raise property damage limits, consider EV-specific coverage, and embrace telematics discounts while being mindful of data privacy.

Common Misconceptions

- “Liability covers my car.” → False. It only covers damage you cause to others.

- “Minimum coverage is enough.” → False. Rising costs make state minimums risky.

- “Umbrella policies are only for the wealthy.” → False. Affordable umbrella coverage can add $1M+ protection.

Key Takeaways

Liability insurance protects your wallet, not your car. In 2026, with higher medical bills and EV repair costs, carrying only minimum coverage is a gamble. Review your policy today — if your limits are below 100/300/100, request a quote to increase them. The extra cost is often less than $10 per month.